The blended brain: why both hemispheres matter when it comes to investing

In a world that often fosters left hemisphere dominance, understanding the differences between our right and left hemispheres may offer a valuable insight into what makes great investors great.

A brief note on this article:

We all have a brain. For investors, it’s a pretty important part of what we do. It’s an organ that is all about connectivity. Tens of billions of neurons and trillions of neuronal connections. So why has the brain, which is all about making connections, evolved to be split in two, a right hemisphere and a left? How and why is this relevant for investors?

It’s not just us humans with our brains partitioned down the middle. All vertebrates—from fish to chimps—have two hemisphere brains. In humans, the brain matter that connects the two hemispheres is called the corpus callosum. The ratio of the corpus callosum to total brain size has been reducing in humans over the years (suggesting less connectivity between the two). In fact, most of the neurons in the corpus callosum have evolved to be inhibitory (i.e. inhibiting the connection between the two hemispheres rather than facilitating connection).

So it looks like evolution has selected for more separation between the two hemispheres rather than less. But why?

The different roles of our brain hemispheres

I have been interested in how the brain works since my early 20s when I struggled to recover from traumatic brain injury. It’s of particular interest to me nowadays given my livelihood and success as an investor is highly dependent on the health and functioning of my brain!

I have known for at least two decades that we have two brain hemispheres. I’ve broadly been aware of the concept that they have evolved to perform different functions. But it wasn’t until last year that the penny dropped—this two hemisphere thing is really important.

The penny dropping is thanks to Dr Iain McGhilchrist. His two books “The Master and his Emissary” and “The Matter with Things” are the culmination of his decades of work and research on brain hemisphere difference. Over three thousand pages citing thousands of references. I stumbled across his work during a seminar on child developmental neurology and the importance of our two brain hemispheres (but that’s a topic for another dad post).

Before I read McGhilchrist’s work, my understanding was that the left hemisphere (“LH”) / right hemisphere (“RH”) distinction revolved around function. For example, language and reason primarily happened in the left and emotion in the right. But that’s not the case. Both sides of the brain are involved in these functional aspects of our lives. The critical difference between the two hemispheres is how they perceive the world and how they draw meaning from it.

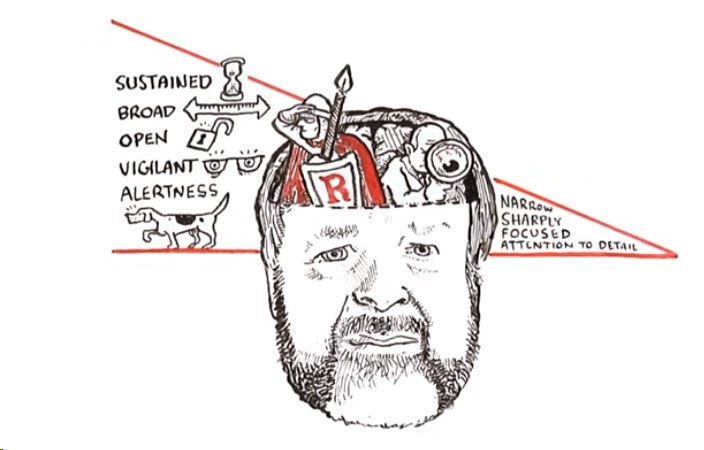

The anecdote McGhilchrist commonly uses to introduce the difference between the two hemispheres is a bird pecking for seeds on the ground amongst grit and pebbles. The bird’s attention needs to be narrowly focused on picking out the seeds in a background of pebbles (using the LH) whilst simultaneously being aware of its surroundings, on the lookout for predators and other relevant circumstantial information (using the RH). The left side of the brain is used for narrow, sharply focused attention to detail. The right side is used for sustained, broad, open, vigilant and alert attention to environment, context, threats and unexpected circumstances.

Image source: RSA ANIMATE: The Divided Brain

This analogy applies to humans also and you can start to see how this applies to successful investing. If I consider our investment process at TDM, we are constantly on the lookout for new opportunities or risks and threats to businesses in our portfolio. Whilst we don’t try to pick the timing of macro cycles, we are environmentally aware—regularly considering if we should be playing “offence or defence”, as Howard Marks would say. These are all activities skewed to the RH.

Simultaneously, we are narrowly focused on our portfolio companies, zeroing in on work specifically relating to them. If we spot a new opportunity, we make the conscious decision to acutely focus on analyzing that business. We analyze the business model and how it makes money. We review the history and track record of the business. We build a financial model. We assess its various competitive advantages. All reasonably concrete, procedural tasks skewed to the LH.

McGilchrist describes the different approaches to seeing the world as “apprehending” (LH) versus “comprehending” (RH). The LH tends to deal with the more certain world. When we already know something is important and want to grasp it (like the bird pecking the seed), we use our LH. It is used to “apprehend”.

When information and meaning are less certain, we use our RH. We use it to “comprehend”. We are taking in a wide range of information in a constantly changing and uncertain environment, looking for patterns and signals.

To use an everyday example from my investing life, when reading an earnings call transcript, my LH will be used to read the words on the page, record the factual information and update our financial model. My RH will be used to comprehend the earnings call in totality; the broader context, the implicit information and what it means from an investment perspective.

So, why does hemisphere difference matter to investors?

I have read so many books and blogs, and listened to so many podcasts that inadvertently focus on how to use the LH—how to break down a competitive advantage or industry structure, theories on valuing businesses, the perils of cognitive biases and the utility of mental models. Seldom have I come across investing content focused on using the RH.

It is very early days in developing my understanding of the role of the left and right hemispheres in investing. However there is little doubt in my mind that strength across both hemispheres is essential to be successful. I sense that most investors are LH dominant. That’s not necessarily a problem but it heightens the importance of understanding and fostering the strengths of the RH.

Like a muscle, spending more time doing LH things reinforces LH strength and vice versa. The vast majority of the investing world is skewed to feed the LH and not the RH. The deluge of data; our ability to build complex models with software; the crude categorisation of companies into buckets that often don’t reflect their uniqueness; and the constant comparison to market indices.

As I worked through McGhilchrist’s thousands of pages I have come to believe that many of the great investors— Buffett, Munger, Marks and others—are distinguished from the rest by the strength of their RH attributes. It’s their ability to see the big picture and not get caught in the detail, their “worldly wisdom” and common sense, their ability to communicate complex ideas using metaphor and storytelling, and their innate “devil’s advocate” that enables them to take in new information and appropriately adjust their views. These characteristics are all the domain of the RH.

Perhaps McGhilchrist’s most important point amongst all his work is contained in the title of his first book: The Master and his Emissary. He emphasises that, whilst both hemispheres are essential and valuable, the RH needs to be in charge. It should be “the master”. The LH should be used as an “emissary”. It should be allocated tasks it is best suited for by the RH.

McGhilchrist argues that there are dire consequences if the LH becomes too dominant. He suggests that so much of the modern world—and I believe this is true of the investing world— is tilted towards valuing and feeding the LH. For investors, this has important implications. Not only would a LH dominant approach to investing miss the immense benefits the RH has to offer but ultimately it would lead to dire consequences in terms of performance.

In my next two articles, as we continue this mini-series about the blended brain, I will delve into some ideas of how the RH plays an essential role in successful investing and how LH dominance could impede performance, using some of the great investors in history as examples. I’ll also suggest some strategies to foster RH strength and purposefully incorporate it into the investment process and life in general.